HOUSE PRICES GO BOTH UP AND DOWN

I originally wrote this post back in 2007, so a lot of the examples and dates are a bit old now – with the benefit of hindsight, it was a bit premature, but still worth keeping in mind in 2022!

House prices go both up and down

When water is boiling in a jug, the hottest water rises to the top, while the coolest water sinks to the bottom. This is an analogy for change of value in the share market, the property market, and many other things. It is a principal of chaos theory, and another way of saying “what goes up must come down”

Jugs of water boil in a few minutes, and then they switch off. Generally it is not expected that they will just keep getting hotter and hotter, yet never explode. And although it’s often forgotten, most share traders maintain some awareness that shares go up and down like sine waves.

For some reason houses are different. Although they too follow a sine wave like pattern that often re-occurs about every 20 years, every time they get really overpriced, it’s as if there is a mass erasure from the collective conscious of all property market history, and the punters are doomed to relive history yet again. I guess the catalyst for this erasure is “greed”

New Zealand house prices are very overvalued, and are long overdue for a crash, but nevertheless there are people saying things like “the NZ housing market won’t crash, it will just flatten out for a while”

As a society we have been conditioned to believe that higher house prices are a good thing, and lower ones bad. In summer it’s hot, and in winter it’s cold, but if we never had a winter everything would be overheated.

PS. House prices in New Zealand did drop in 2008-2009, but they have gone up massively since then. House prices in New Zealand are some of the highest in the world.

To deny that house prices go both up and down is so closed minded as to be bizarre. I’m not judging it as good or bad that house prices go down sometimes, I’m just stating something fairly obvious – sometimes house prices go down. This housing roller coaster video shows it pretty well.

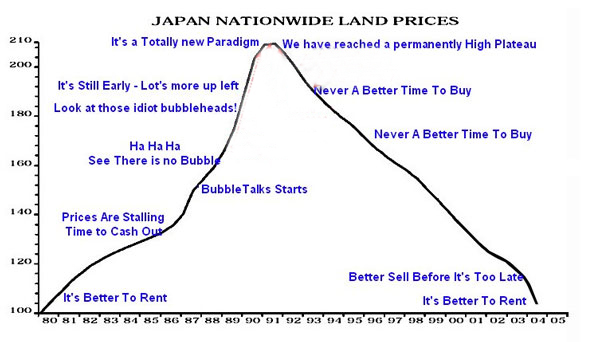

Oddly enough, despite the fact that NZ is geographically similar to Japan, and nearly all the cars here come from Japan, any mention of the 90’s Japanese housing crash brings blank stares.

Basically the Japanese housing market got very overheated in the 80’s, and crashed in 1991. There is nothing unusual about that, as housing markets tend to drop about every 20 years. But the difference in this case it never really recovered.

“If something can’t go on forever, it won’t.”

– Stein’s Law

“If something unsustainable goes on for a while, there will be people claiming it can go on forever.”

– Glassman’s Law

Houses only go down in America, never in NZ

This kind of thing could never happen in New Zealand!

“Today’s property was purchased on 16/10/2006 for US$869,000 and sold at auction on 27/9/2007 for US$682,763. These are not asking prices, these are actual transaction amounts. That is a 21.4% loss in less than one year, and that is not including any transaction costs”

America is completely different to NZ – we are not so gullible and easily mislead!

Here’s a real life example from Wellington, New Zealand – a house was put on market for $550,000 in 2008 – there was no interest from buyers, so after 6 months it had $50,000 of upgrades done to it to attract buyers, and the price was reduced to $500,000.

Still no interest, so it was reduced to $450,000 ono. In 2007 it would have sold for the $550,000 as it was, but by mid 2009 when it was taken off the market, it was not even able to attract an offer over $400,000, even after having had $50,000 of improvements – so that’s drop in value of $200,000 (a 33% drop) in 18 months – but as it never sold, officially none of this ever took place.

And this must be a misprint….

“In NZ the average sale price fell to $393,198 in November, from $406,176 in October – that’s a 3.2% drop in one month, which would be 38% per year”

– December 2007

NZ is much less overvalued…really…

For some strange reason people in England keep talking about our housing market – what would they know?

“The special report from Fitch Ratings also named the UK as having the second most overvalued house prices, behind France.

It said the UK, Denmark and New Zealand were the countries most exposed to economic problems if property prices weakened and interest rates rose.

Fitch, which judges how risky debt is for the City, highlighted how house prices had massively outstripped incomes in Britain over the past ten years.

According to Halifax’s June house price figures, the average home in the UK has risen to £196,500, compared to £68,000 in 1997.

Meanwhile, the most recent figures from the Office of National Statistics said the gross median salary had risen from £16,700, in 1997, to £23,250 in 2006.

Brian Coulton, of Fitch, said: ‘Given record levels of household debt, rising interest rates and after several years of strong house price inflation in many countries, Fitch has assessed a range of indicators of household balance sheet vulnerabilities and house price valuation measures.

‘For overall vulnerability, New Zealand ranks first, Denmark second and the UK third as the most exposed countries. Japan, Germany and Italy are the least vulnerable’

The report added that France was the most exposed country to housing overvaluation, followed by UK, Denmark and New Zealand, which all exhibited the most vulnerable rankings”

They are all just doom merchants, NZ house prices could never go down.

“The current housing boom is unusual not just in its degree of deviation from the long-term trend (which roughly equals three previous peaks) but also in the length of time it has spent trading at a level which has previously quickly triggered a decline”

“The UK also has its own Trojan horse in the shape of buy-to-let investors. The proportion of let properties has not increased significantly above its long-term average of about 10%. What has changed has been a shift from relatively professional landlords to gullible and inexperienced amateurs. All the anecdotal evidence supports the view that the ‘smart money’ – hardened investors with previous cyclical experience, has been pulling out for some time already”

As the chart shows, on the conventional measure of value, the ratio of average house prices to average earnings, the market already looks strained to breaking point. Of course, this measure has been widely attacked as irrelevant. And, over recent years, it has certainly been a poor indicator – so far. But this has been because of three key factors – the shift to very low interest rates, the relaxation of lending criteria and the growth of the buy-to-let market. I suspect that these factors will no longer be able to bail out the market.

Many borrowers have so far been insulated from these moves by fixed-rate deals which will now be expiring, forcing them to refinance at higher rates. Moreover, because of the change in the credit markets brought about by this summer’s liquidity crisis, even at the same level of official interest rates the rates on offer to borrowers are likely to be higher. And the supply of fancy mortgages with very high multiples of earnings, or of the property’s purchase price, will have dried up.

In any case, the big story in the housing market has been about the rise in affordability made possible by the sharp drop in interest rates in this decade compared with what had gone before. This made it possible for people to afford a much bigger mortgage even when house prices were much higher multiples of their earnings than previously. But house prices have risen so far that the boost to affordability from lower interest rates has already been more than exhausted. The proportion of an average new buyer’s after-tax income taken up by mortgage payments is now 50pc, the highest it has been since the dark days of 1990.

So why has the market continued to be so strong? This is where buy-to-let comes in. The growth of the buy-to-let market brought in buyers who were not governed by considerations of affordability. What drove them was investment returns. And these have been tremendous.

But house prices have now risen so far in relation to rents that the yield on property is now well below the cost of finance. In order to expect a decent return, you have to believe that prices are going to continue rising.

Dependence upon this factor makes the market precarious. If house prices start to go down, then even if most buy-to-let investors stay put, new ones will not readily appear and this itself will become the source of further falls in prices. Meanwhile, prospective investors are going to find finance much more difficult and expensive to come by. Accordingly, this time round it is surely difficult to envisage another surge of buy-to-let investors willing and able to replace owner-occupiers frozen out by the unaffordability of houses.

So is there going to be a housing market “crash”? No. Stockmarkets may crash but housing markets don’t. Indeed, even when prices are significantly too high, as they may well be now, the first reaction is for the market to freeze up rather than for prices to fall. Even later, the inhibitions to falling prices are quite severe. In the housing market, prices dribble lower rather than plunge. That is what I suspect may happen next year and for a good while to come.

Roger Bootle – 16/10/2007

US Housing Crash Continues – Why it’s A Terrible Time To Buy

1. Prices still disconnected from fundamentals. House prices are still far beyond any historically known relationship to rents or salaries. Yearly rents are 3% of purchase price. Mortgage rates are 6.5%, so it costs more than twice as much to borrow money to buy a house than it does to rent an equivalent house. Worse, total owner costs including taxes, maintenance, and insurance are about 9%, which is three times the cost of renting. Salaries cannot cover mortgages. Anyone who buys now will suffer losses immediately, and for the next several years at least.

2. Buyers borrowed too much money and cannot pay the interest. Now there are mass foreclosures, and senators are talking about taking your money to pay for your neighbor’s McMansion.

Banks happily loaned whatever amount borrowers wanted as long as the banks could then sell the loan, pushing the risk onto Fannie Mae (ultimately taxpayers) or onto buyers of mortgage backed securities. Now that it has become clear that a trillion dollars in mortgage loans will not be repaid, Fannie Mae is under pressure not to buy risky loans and investors do not want mortgage backed securities. This means that the money available for mortgages is falling, and house prices will keep falling, probably for 5 years or more. This is not just a subprime problem. All mortgages will be harder to get.

3. Interest rates increases. When rates go from 5% to 7%, that’s a 40% increase in the amount of interest a buyer has to pay. House prices must drop proportionately to compensate. The housing bust still has a very long way to go.

For example, if interest rates are 5%, then $1000 per month ($12,000 per year) pays for an interest-only loan of $240,000. If interest rates rise to 7%, then that same $1000 per month pays for an interest-only loan of only $171,428.

Even if the Fed does not raise rates any more, all those adjustable mortgages will go up anyway, because they will adjust upward from the low initial “teaser” rate to the current rate.

4. Extreme use of leverage. Leverage means using debt to amplify gain. Most people forget that losses get amplified as well. If a buyer puts 10% down and the house goes down 10%, he has lost 100% of his money on paper. If he has to sell due to job loss or an interest rate hike, he’s bankrupt in the real world.

It’s worse than that. House prices do not even have to fall to cause big losses. The cost of selling a house is 6%. On a $300,000 house, that’s $18,000 lost even if prices just stay flat. So a 4% decline in housing prices bankrupts all those with 10% equity or less.

5. Shortage of first-time buyers. High house prices have been very unfair to new families, especially those with children. It is literally impossible for them to buy at current prices, yet government leaders never talk about how lower house prices are good for most people, instead preferring to sacrifice American families to make sure bankers have plenty of debt to earn interest on. Every “affordability” program has the effect of driving prices higher and locking out more middle-class people. To really help Americans, Fannie Mae and Freddie Mac should be completely eliminated.

6. Surplus of speculators. Nationally, 25% of houses bought in 2005 were pure speculation, not houses to live in, and the speculators are going into foreclosure in large numbers now. Even the National Association of House Builders admits that “Investor-driven price appreciation looms over some housing markets.”

7. Fraud. It has become common for speculators take out a loan for up to 50% more than the price of the house he intends to buy. The appraiser goes along with the inflated price, or he does not ever get called back to do another appraisal. The speculator then pays the seller his asking price (much less than the loan amount), and uses the extra money to make mortgage payments on the unreasonably large mortgage until he can find a buyer to take the house off his hands for more than he paid. Worked great during the boom. Now it doesn’t work at all, unless the speculator simply skips town with the extra money.

8. Baby boomers retiring. There are 77 million Americans born between 1946-1964. One-third have zero retirement savings. The oldest are 61. The only money they have is equity in a house, so they must sell.

9. Huge glut of empty housing. Builders are being forced to drop prices even faster than owners. Builders have huge excess inventory that they cannot sell, and more houses are completed each day, making the housing slump worse.

10. The best summary explanation, from Business Week: “Today’s housing prices are predicated on an impossible combination: the strong growth in income and asset values of a strong economy, plus the ultra-low interest rates of a weak economy. Either the economy’s long-term prospects will get worse or rates will rise. In either scenario, housing will weaken.”

“In my view, a sub-prime-fuelled housing market crash in the UK is extremely unlikely — in fact, just about as likely as a Martian invasion.”

Donna Werbner, News Editor of yourmortgage.co.uk – October 2007

This time last year we had 80 properties to sell and now we have 240. There are too many houses and not enough buyers. We are having to reduce prices. A house that might have sold at £290,000 last year will be put on the market this year at £250,000 and still struggle to sell.”

Alan Emery, Ocean Estate Agents – October 2007